“ABC is on the rise: trust me, i'm on it” The Filter^ 2006)

This post surveys how ABC has been treated in the mainstream media from the period of the “great moderation” through to around Summer 2010. (The reason for stopping here is because media coverage has become so widespread it would warrant a move from qualitative methods to more quantitative ones). Many of the examples used are not the result of retrospective research, for example on September 7th 2006 I posted a round up of increasing attention to ABC. The aim is to use archival sources to bridge the gap between ABC as a fringe school of thought, to becoming a widely discussed and publicly well known set of ideas.

It would be wrong to pretend that Austrian economics has become a widespread and recognised alternative to the Keynesian consensus, but it is important to note the dramatic and telling increase in exposure. We do need to be careful about over reaching. Therefore this paper does not rely on statements that can merely be interpreted through the lens of Austrian economics (and are thus “claimed” as Austrian). For example John Taylor wrote the following in the Wall Street Journal:

“A housing boom followed by a bust led to defaults, the implosion of mortgages and mortgage-related securities at financial institutions, and resulting financial turmoil… Monetary excesses were the main cause of the boom. The Fed held its target interest rate, especially in 2003-2005, well below known monetary guidelines that say what good policy should be based on historical experience… The greater the degree of monetary excess in a country, the larger was the housing boom”

Such an explanation seems highly compatible with the Austrian story, and is one of a number of similar examples (for example Anna Schwartz and Jeffrey Sachs could also be deemed to have relied upon “Austrian” explanations). However we will limit our survey to articles that require no interpretation, in other words articles that explicitly mention the Austrian school. And indeed we needn’t rely on a retroactive response to the financial crisis – there is evidence that the Austrian school provided advanced warning and that this was known amongst the mainstream media.

Consider for example three articles that appeared in The Economist in 2002, 2003 and 2005 (i.e. before the collapse of the subprime mortgage market in the summer of 2007, the bankruptcy of Lehman Brothers in September 2008, and the resulting global recession). Firstly, they suggest that ABC may become more common:

“the Austrian cycle may become more common again if, as this survey will argue, financial liberalisation has made bubbles in credit and investment more likely”

One year later they reiterate the benefits of understanding ABC

“perhaps it is a good time to dust down Austrian business-cycle theory… America displayed many of those [Austrian] features in the late 1990s. Faster productivity growth raised the natural rate of interest, but because inflation was low (and because Austrian economics had long been out of fashion) the Fed failed to lift interest rates by enough. Investment and borrowing boomed.”

Then in June 2005 they correctly linked these prior warnings to the pending recession:

“No wonder that the Federal Reserve is starting, belatedly, to fret about house prices. By holding interest rates low for so long after equities crashed, the Fed hoped to inflate house prices. This prevented a deep recession, but it may have merely delayed the needed economic adjustment.”

When the structural problems within the economy began to manifest in 2006 three different newspapers directly invoked Austrian economics. Kaushik Das (an economist with SBI Capital Markets Ltd) wrote in the Financial Express:

“the Austrian Business Cycle theory can be very well applied to explain the current global as well as domestic financial imbalances”

According to John Dizzard, in the Financial Times,

“The Fed, with the encouragement and support of the political class, kept rates low so as continually to postpone financial busts over the past decade and a half… The Austrian analysis is probably the best one on hand to analyse the present bind of investors and central bankers”

And then The Economist, also:

“A more relevant model might be one based on the Austrian school of economics, developed in the late 19th century, when economic conditions were more akin to today's. In Austrian models the main result of excessively low interest rates is not inflation but over borrowing, an imbalance between saving and investment and a consequent misallocation of resources. That sounds like America today.”

Once history began to catch up with theory, a number of major broadsheet newspapers published opinion editorials that present ABC as the prime explanation of the crisis. George Bragues writing for The Financial Post ("Paulson's scheme", October 7th 2008) said,

"To the extent that this assessment has been made, it represents an important victory for a school of thought that has long hung on the margins of the economics discipline: the Austrian school of economics, whose most illustrious figures include the Nobel prize winning Friedrich von Hayek and Ludwig von Mises. Austrian economists hold that downturns are the inevitable aftermath of loose monetary policy, thus opposing explanations typically heard prior to the current crisis that attributed recessions to price shocks, underconsumption or central bank tightening of monetary policy"

Andrew Lilico wrote a Guardian column that provided an introduction to the Austrian school and the possible necessity for malinvestment to be liquidated.

John Authers in The Financial Times focused on Ludwig von Mises in particular,

“For von Mises, government is the danger, and is never justified in interfering with the market… For followers of von Mises, the expansive monetary and fiscal policy that has followed the crisis is wrong. They would advocate a drastic paring back in regulation and the removal of discretion from central banks. Presumably, as they hold that the market would not allow institutions to become too big to fail in the first place, they would support some kind of intervention to make the biggest banks smaller”

Dick Armey in the Wall Street Journal drew attention to FA Hayek,

“"Hayek, who famously debated Keynes in a series of articles after the release of "General Theory," gave what I believe to be the most devastating critique of government action to stimulate "aggregate demand." Hayek viewed the boom and bust of the business cycle as primarily a monetary phenomenon created by governments' artificial inflation of money and credit."

And in the New York Times, Kyle Crichton drew upon Hayek and modern proponents such as Peter Schiff,

“Austrian economists tend to emphasize a laissez-faire approach and entrepreneurship (not the most popular policies at this moment) and strict limits on money supply growth, usually by hitching the currency to the gold standard. While considered outside the mainstream, the Austrian School is far more respectable, counting in its ranks two Nobel Prize winners, Friedrich Hayek and James Buchanan. Peter Schiff of Euro Pacific Capital — an adviser to the libertarian presidential candidate Ron Paul and one of the most prominent doomsayers in the current collapse — also subscribes to its theories. Hayek is said to have successfully predicted the Great Depression and some Austrian School devotees are taking credit for calling this one. “The financial meltdown the economists of the Austrian School predicted has arrived,” Mr. Paul wrote in September, 11 days after Lehman Brothers filed for bankruptcy”

Indeed the influence and rise of Ron Paul has led to the previously unthinkable situation where the motto “End the Fed” appeared in the Financial Times,

“At marches and meetings against big government across the US, where some placards damn the president, others bear a catchy slogan: "End the Fed”… For Mr Paul and his allies, removing the Fed would end almost a century of rule over the economy by an undemocratic institution that has weakened the dollar and stoked inflation.”

It is telling to note that as part of the debate about how to respond to the financial crisis three of the UK’s most respected broadsheet newspapers – The Guardian, The Financial Times, and The Times published articles by prominent columnists discussing ABC and Austrian economics more generally. Writing in The Guardian, economics editor Larry Elliott (whilst not endorsing it) refers to the Austrian school as “clear and consistent.” Martin Wolf, the Financial Times’ chief economics commentator, said that he had sympathy with the Austrian view, pointing to the notion that “inflation-targeting is inherently destabilising; that fractional reserve banking creates unmanageable credit booms; and that the resulting global “malinvestment” explains the subsequent financial crash.” (see here for a rejoinder to Wolf's article). And finally, The Times’ Editor-at-large Anatole Kaletsky referred to the Austrian school as “seemingly common-sense” (albeit then concluding that “it makes no sense”!) (see here for a rejoinder to Kaletsky).

But the point remains that it is deemed worthy of dismissing, and thus discussing. There can be little doubt that exposure to Austrian ideas has increased. Indeed when I was first attempting to write opinion editorials I was advised not to use distinctly Austrian terms such as “malinvestment” since they were little known and signalled being an unorthodox concept. And yet The Economist now regularly uses the term as it has entered the popular lexicon (here and here).

The financial crisis put paid to a vast array of ventures, but Austrian economics has emerged all the stronger.

Addendum: Two more:

Taking von Mises to pieces, The Economist

A one-paragraph explanation of the Austrian theory of business cycles would run as follows. Interest rates are held at too low a level, creating a credit boom. Low financing costs persuade entrepreneurs to fund too many projects. Capital is misallocated into wasteful areas. When the bust comes the economy is stuck with the burden of excess capacity, which then takes years to clear up.

Jailed counterfeiters aren't a patch on the Bank of England, Jeff Randall, The Telegraph

The regulators are praying that the rest of us won’t notice. This is a high-wire act. As the economist Ludwig Von Mises noted, when the masses finally wake up, “a breakdown occurs”.

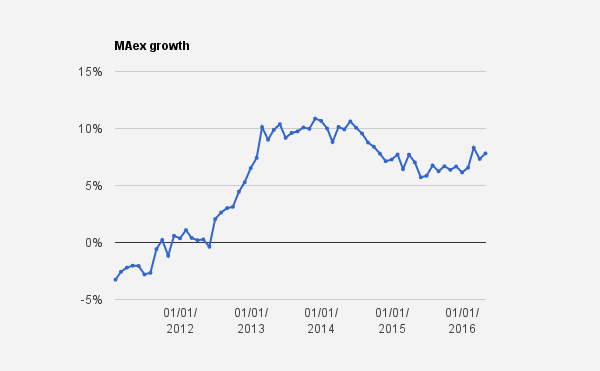

In 2006 it was growing at 7.88% which indicated an even larger boom that was being shown in NGDP data (which grew by 5.52%). It then contracted by -2.31% in 2009 before picking up again. As with NGDP the post crisis growth rate seems enduringly lower. My main interest was the 2014 figure, and we can see that whilst Gross Output grew faster than NGDP in 2013, this was reversed in 2014. Whilst NGDP delivered a robust 4.77%, Gross Output only grew by 3.49%.

In 2006 it was growing at 7.88% which indicated an even larger boom that was being shown in NGDP data (which grew by 5.52%). It then contracted by -2.31% in 2009 before picking up again. As with NGDP the post crisis growth rate seems enduringly lower. My main interest was the 2014 figure, and we can see that whilst Gross Output grew faster than NGDP in 2013, this was reversed in 2014. Whilst NGDP delivered a robust 4.77%, Gross Output only grew by 3.49%.